Application Requirements

Non-resident enterprises that have incorporated under foreign law without actual institutions of management in China but have institutions or establishments inside China shall submit an annual enterprise income tax return to the tax authority within five months from the end of a tax year and settle the payable and refundable tax; where an enterprise terminates its business activities during a tax year, it shall, within 60 days from the date it actually terminates its business operation, settle its enterprise income tax of the current period on a consolidated basis with the taxation authority.

Legal Basis

1. Article 25, Paragraph 1 of the Law on Administration of Taxation of the People’s Republic of China

2. Article 3, Article 54 Paragraph 3, and Article 55 Paragraph 1 of the Enterprise Income Tax Law of the People’s Republic of China

3. Interim Measures for the Administration of Taxation on Contracting for Engineering Work and Provision of Labor Services by Non-Residents (Decree No. 19 of the State Taxation Administration)

4. State Taxation Administration (STA) Notice on Issuing the Interim Measures for the Administration of Taxation on Permanent Representative Offices of Foreign Enterprises (Guo Shui Fa [2010] No. 18)

5. State Taxation Administration (STA) Notice on Issuing the Administrative Measures for the Assessment and Levy of Enterprise Income Tax on Non-resident Enterprises(Guo Shui Fa [2010] No. 19)

6. State Taxation Administration (STA) Public Notice on Issuing the Interim Measures for the Administration of Taxation on Non-Resident Enterprises Engaging in International Transport Business (STA Public Notice [2014] No. 37)

7. State Taxation Administration (STA) Public Notice on Amending the Administrative Measures for the Assessment and Levy of Enterprise Income Tax on Non-resident Enterprises and Other Documents (STA Public Notice [2015] No. 22)

8. State Taxation Administration (STA) Public Notice on Issuing the Administrative Measures for Non-Resident Taxpayers Claiming Tax Treaty Benefits (STA Public Notice [2015] No. 60)

9. State Taxation Administration (STA) Public Notice on Issuing the Tax Return Form of the People’s Republic of China for the Prepayment of Non-resident Enterprise Income Tax (2019 Version) and Other Forms (STA Public Notice [2019] No. 16)

Materials Needed

Notes:

1. Taxpayers are responsible for the authenticity and legality of the materials submitted.

2. Taxpayers are required to submit paper documents when they go to the tax service hall to handle their tax affairs,or submit electronic documents according to the operation requirements of the online system if they handle their tax affairs online or through mobile terminals.

3. For materials not specified as original or printed copies in the “Materials Needed” list, the original copies shall be provided; for materials specified as printed copies, only printed copies shall be provided; for materials specified as original and printed copies, the printed copies will be collected, and the original copies will be returned after verification.

4. The submitted printed copies must state its consistency with the original copies and be stamped with the company’s official seal.

Service Channels

1. Tax Service Halls (Click to view the location, opening hours and contact information of the tax service halls)

“City-wide Universal Processing” services will be provided at all tax service halls except for the Second Tax Bureau of Shenzhen Municipality.

2. A self-service tax terminal is available.

3. Online service

An E-tax bureau service is available. (e-tax bureau)

Mobile terminal (tax bureau) and WeChat (tax bureau) are not available.

Processing Authority

The competent tax authorities

Processing Time

1. Time limit for taxpayers

An annual enterprise income tax return shall be submitted within five months from the end of a tax year or within 60 days from the date the enterprise terminates its business operation if it terminates its business activities during a tax year.

2. Time limit for tax authorities

If the materialssubmitted are complete and conform to the legal form and the content filled is complete, the tax authority shall complete the procedure immediately after acceptance.

Please refer to the tax service map for contact numbers of each tax service hall.

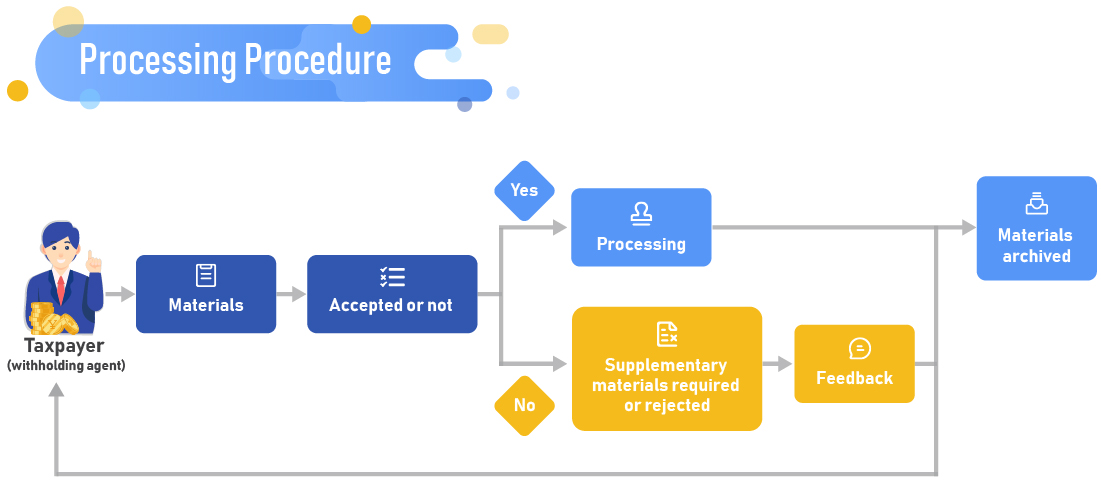

Processing Procedure

Processing Result

Tax authorities will give feedback on the Tax Return Form of the People’s Republic of China for Annual Non-resident Enterprise Income Tax (2019 Ver.).

Notices for Taxpayers

1. The tax authorities provide single-window service. Taxpayers need to visit the tax authorities only once at most on the precondition that the materials are complete and meet the legal requirements for acceptance.

2. Taxpayers may use e-signatures that meet the requirements of the Electronic Signature Law of the People’s Republic of China, which has the same legal effect as handwritten signatures or seals.

3. The submitted printed copies must state its consistency with the original copies and be stamped with the company’s official seal.

4. Taxpayers shall file tax returns in accordance with the relevant regulations, regardless of the taxpayer’s profit or loss status in the business year.

5. Before filing an annual tax return, taxpayers should complete the filing of tax returns for the quarterly prepayment of enterprise income tax for the whole year.

6. Taxpayers who fail to file tax returns and submit the required materials in accordance with the prescribed deadlines shall bear the corresponding legal responsibilities in accordance with the relevant provisions of the Law on Administration of Taxation of the People's Republic of China.

7. If a non-resident enterprise contractsfor engineering work or provides labor services in China, it shall, within 30 days from the date of signing the project contract or agreement, file the tax registration procedure with the competent tax authority in the project location.

8. Non-resident enterprises engaged in international transportation business that have already registered for taxation shall declare to the competent taxation authority in the place where it registered with to pay enterprise income tax according to relevant laws and regulations.

9. Non-resident enterprises that have set up institutions and establishments in China and have filed their annual enterprise income tax returns with the tax authorities shall file related declarations regarding their business transactions with related parties.

10. Before theTax Return Form of the People’s Republic of China for Annual Non-resident Enterprise Income Tax (2019 Ver.) is officially put into use, the Tax Return Form of the People’s Republic of China for Quarterly and Annual Non-resident Enterprise Income Tax (applicable to paying on a deemed basis) / (not constituting tax exemption declaration for permanent establishment and international transportation) or Tax Return Form of the People’s Republic of China for Annual Non-resident Enterprise Income Tax (applicable to payments on an actual profit basis) shall be used as required.

Fees

Free of charge

Application Forms

The form can be downloaded from the “Tax Services” – “Download Center” – “Form Download” section of the Shenzhen Tax Service website, State Taxation Administration (specific download address) or collected from the tax service halls.

Instructions for Filling out Forms

Please see the instructions for filling out as shown in the relevant forms.