Application Requirements

Non-resident taxpayers with tax liabilities in China who have self-assessed that they are eligible for the treaty benefits can claim such tax treaty benefits accordingly by self-filing or by filing through the withholding agents on withholding at source provided that they have collected and retained relevant supporting documents for inspection for the tax authorities in their post-filing administration process.

Legal Basis

Article 3 of the State Taxation Administration (STA) Public Noticeon the Issuance of the Administrative Measures for Non-Resident Taxpayers Claiming Tax Treaty Benefits (STA Public Notice No.35, 2019).

Materials Needed

Notes:

Non-resident taxpayers shall bear legal responsibility for the authenticity, accuracy and legality of the information filled in the Reporting Form for Non-resident Taxpayers Claiming Tax Treaty Benefits and the supporting documents retained for future inspection. The withholding agent shall withhold tax according to the preferential treatments based on the Reporting Form filled out by the non-resident taxpayer, while the non-resident taxpayer shall still be responsible for the authenticity of the Reporting Form and retaining supporting documents for post-filing inspection.

Service Channels

1.Tax Service Halls (Click to view the location, opening hours and contact information of the tax service halls)

“City-wide Universal Processing” services will be provided at all tax service halls except for the Second Tax Bureau of Shenzhen Municipality: Yes

2. Self-service terminal: No

3. Online service

E-tax bureau: No (e-tax bureau)

Mobile terminal (tax bureau): No

WeChat (tax bureau): No

Processing Authority

Tax authorities

Processing Time

The tax authority shall conclude the procedure immediately after acceptance.

Tel.

Please refer to the tax service map for contact numbers of each tax service hall.

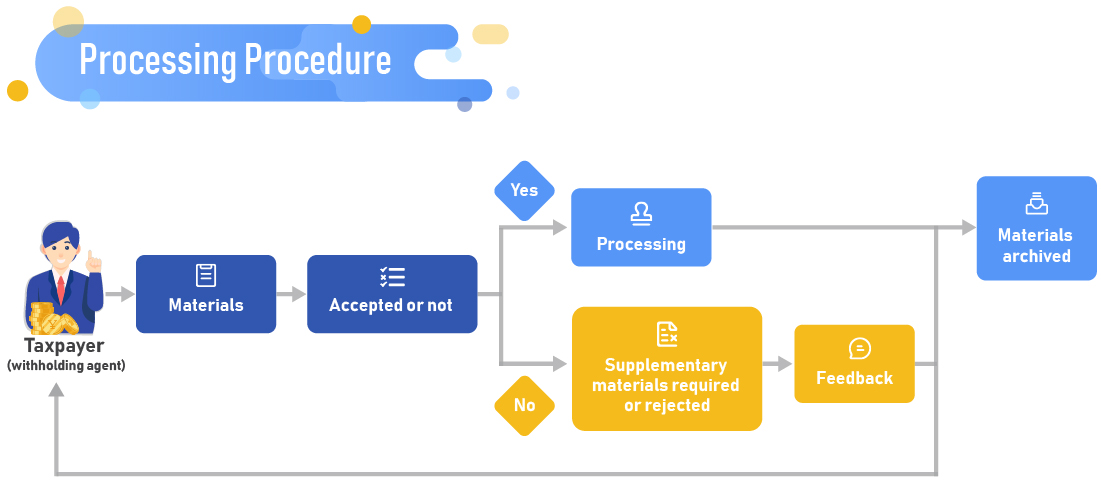

Processing Procedure

Processing Result

Tax authorities will give feedback on the processing result.

Notices for Taxpayer

1. The tax authorities provide single-window service. Taxpayers need to visit the tax authorities only once at most on the precondition that the materials are complete and meet the legal requirements for acceptance.

2. The tax reduction and exemption item codesinvolved in this item includes 04135401, 04135501, 04135601, 04135701, 04139901, 05135401, 05135501, 05135601, 05135701 and 05139901.

3. Non-resident taxpayers can enjoy tax treaty benefits via the “self-assessment of eligibility, claiming treaty benefits, retaining documents for inspection” mechanism. Non-resident taxpayers who have self-assessed that they are eligible for the treaty benefits can claim such tax treaty benefits accordingly on self-filing or through the withholding agents on withholding at source provided that they have collected and retained relevant supporting documents for inspection by the tax authorities in their post-filing administration process.

4. The “treaties” referred to therein include tax treaties and international transport treaties. International transport treaties include air transport agreements, maritime transport agreements, road transport agreements, motor transport agreements,agreements or letters for mutual exemption of tax on international transport income, and other agreements on international transport signed by the Government of the People’s Republic of China.

The “treaty benefits” referred to therein refers to the tax treatments under which the corporate income tax and personal income tax that should be paid under domestic tax laws can be reduced or exempted for eligible non-resident taxpayers according to the relevant treaties.

The “withholding agent” referred to therein refers to the entity or individual who is obligated to withhold tax on non-resident taxpayers’ China-source income and submit the requisite payment to tax authorities according to the domestic tax laws, including the statutory withholding agent and the designated withholding agent under the Enterprise Income Tax Law.

5. For non-resident taxpayers claiming treaty benefits based on the arrangement for avoidance of double taxation signed between the Mainland of China and China’s Special Administrative Regions of Hong Kong and Macao, the reporting shall be conducted as stipulated in this item.

6. Non-resident taxpayers claiming treaty benefits shall retain the following documents for future inspection.

(1) The Tax Resident Certificate issued by the in-charge tax authorities of the other contracting jurisdiction under the relevant tax treaty that proves the tax resident status of the non-resident taxpayer for the current year or the previous year in which the non-resident taxpayer obtained the income; for non-resident taxpayers claiming tax treatments based on the international transport clause of tax treaties or the international transport treaties, certificates that can prove the eligible status of the non-resident taxpayer under the relevant treaties may be used instead of the Tax Resident Certificate.

(2) Contracts, agreements, board of directors’ or shareholders’ meeting resolutions, payment certificates and other documents proving ownership related to the acquisition of relevant income.

(3) Relevant materials to justify “beneficiary owner” status under the treaty article of dividends, interest, or royalties.

(4) Other information that the non-resident taxpayer believes can provetheir eligibility for the treaty benefits.

7. If a non-resident taxpayer fails to provide the Reporting Form for Non-resident Taxpayers Claiming Tax Treaty Benefits to the withholding agent or the Reporting Form provided is incomplete, the withholding agent shall withhold tax based on the domestic tax laws.

8.If a non-resident taxpayer discovers that they had enjoyed treaty benefits that they are not entitled to and resulted in tax underpayment, the non-resident taxpayer shall take the initiative to report underpaid tax to the tax authority and settle the payment.

9. If a non-resident taxpayer fails to enjoy treaty benefits thatthey are entitled to and resulted in tax overpayment, within the period stipulated in the Law on Administration of Taxation of the People's Republic of China may request the competent tax authority to refund the overpayment of tax by themselves or through the withholding agent, and submit relevant materials at the same time.

10.Non-resident taxpayers shall retain the relevant materials on their eligibility to enjoy treaty benefits for future inspection for a certain period as specified in the Law on Administration of Taxation (LAT) and Rules for the Implementation of LAT.

11. Non-resident taxpayers and withholding agents shall cooperate with the competent tax authorities in post-filing administration and investigation on non-resident taxpayers claiming tax treaty benefits.

12. In the post-filing administration process, the competent tax authorities may require the non-resident taxpayers to provide the retained documents for inspection within a certain period.

13. If the original retained document is ina foreign language, it should be accompanied by a Chinese translation when it is provided at the request of the competent tax authority, and the non-resident taxpayers shall be responsible for the accuracy and completeness of the Chinese translation.

Non-resident taxpayers and withholding agents may provide printed copies of the required materials to the competent tax authorities, but it should be specified on the printed copiesthe location where the originals are stored, and be sealed or signed by the person responsible for the reporting. If the tax authorities require the original documents, the original documents shall be provided.

Fees

Free of charge

Application Forms

The Reporting Form can be downloaded from the “Tax Services” – “Download Center” – “Form Download” section of the Shenzhen Tax Service website, State Taxation Administration (specific download address) or collected from the tax service halls.

Instructions for Filling out Forms

Please see the instructions for filling out as shown in the relevant forms.